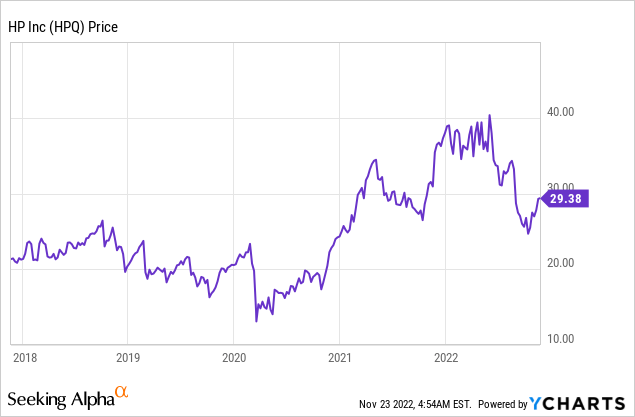

BalkansCat

HP Inc.NYSE:HPQ() is a technology company with a long history that sells Personal Computers and Printers. The company is currently facing headwinds due to the cyclical decline of the personal computing market. The business will still benefit long-term from the cyclical decline in personal computing market. Trends such as remote work (after Poly’s acquisition, which will be discussed later) or 3D printing are some of the most important growth trends. In 2021, the global 3D printing market was worth $13.8 billion. Prognosticated To grow at a rapid 20.8% compounded annually growth rate up 2030. Let’s get into the financial results and reveal HP’s valuation in this post.

Fourth Quarter Financial Results

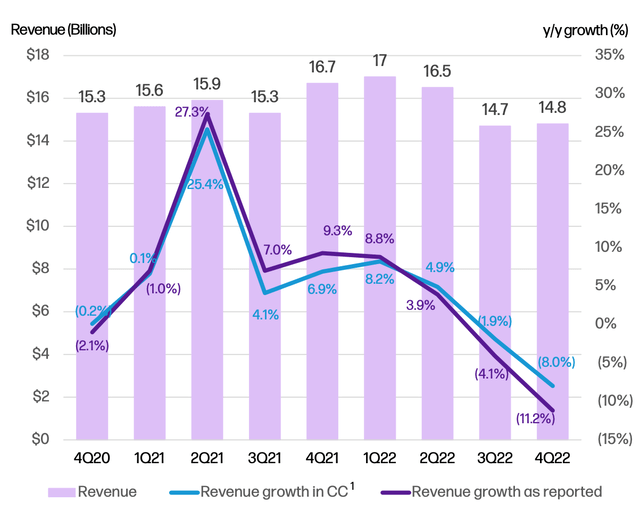

For the fourth quarter fiscal year 2022, HP posted solid financial results. Analyst expectations were $124 million higher than the revenue of $14.8 billion. Revenue declined by 11% over the year, or 8%, on a constant currency basis. Management expected this to be due to macro headwinds.

Revenue HPQ (Q4 Earnings Review)

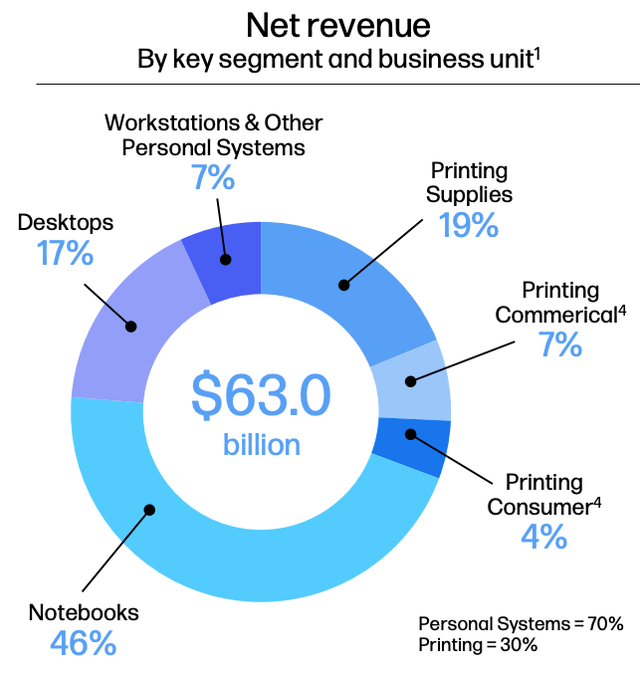

The majority of HP’s revenue comes from Personal Systems Revenue (70%) and Printing revenue (30%). Personal Systems revenue decreased by 9% year over year but rose sequentially by 4% using constant currency. It reached $10.3 billion in F22 quarter. The Personal Systems segment can be further broken down into Notebooks (46% of revenue), Desktops (17%), and Workstation & Other systems (7%).

The market is currently experiencing a cyclical downturn, which has led to a drop in demand for consumer computers. There are a few reasons for this. First, computers and gaming saw a huge increase in sales during 2020’s lockdown. This was because so many people were at home, and it was popular to set up home offices for remote work. Stimulus check programs all over the world made many people “cash-rich”.

But the environment will be completely different in 2022. High inflation and rising interest rates are putting pressure on both consumers and businesses. This is leading to higher input costs for both consumers and businesses. Despite this macroeconomic environment HP continues to innovate. In fact, HP announced a new line of gaming and notebook computers at the CES Event 2022.

Poly, which is a provider videoconferencing solutions that include headsets, microphones, software, and cameras, was also acquired by the company. Its acquisition cost $3.3 billion. Poly-derived financials were included in the fourth quarter results, which include two months of Poly’s financials. Management has said that Poly is performing “better then expected”. This is understandable given the increase in hybrid working and the efficiency of this work. One study found that 63% of high-revenue growth businesses use hybrid workforce models.

The positive trend in HP’s Personal Systems division is a positive step towards more commercial business. This segment accounts for 75% of the revenue. This is a great trend to see. Commercial businesses tend have higher order volumes and more repeat orders.

Segment by Segment: Net Revenue (Q4 2022)

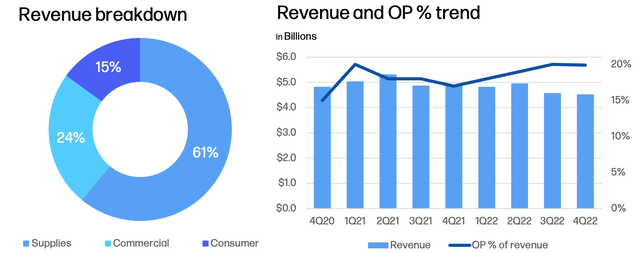

The Print segment saw revenue of $4.5 billion. This was a decrease by 7% or 6% year-over-year. The Consumer market’s softness was responsible for this decline. The need for physical printers is less than it was 10-20 years ago, due to digital technology and Esign (electronic signing) services.

Based on my own experience, an HP printer I purchased five years ago is the one I actually use for postage labels. The user experience is poor. I prefer QR code-based postage labels. The good news for HP: the commercial business has experienced a strong recovery from the pandemic. Revenues from hardware recovery have increased by double digits each year.

HP+ and Big Tank printers are responsible for 55% HP’s printing sales. The quarter saw strong 3D printing, and Industrial graphics sales, which are all increasing year-over-year.

Print Segment Revenue (Q4, F22 Earnings Review)

Profitability and Expenses

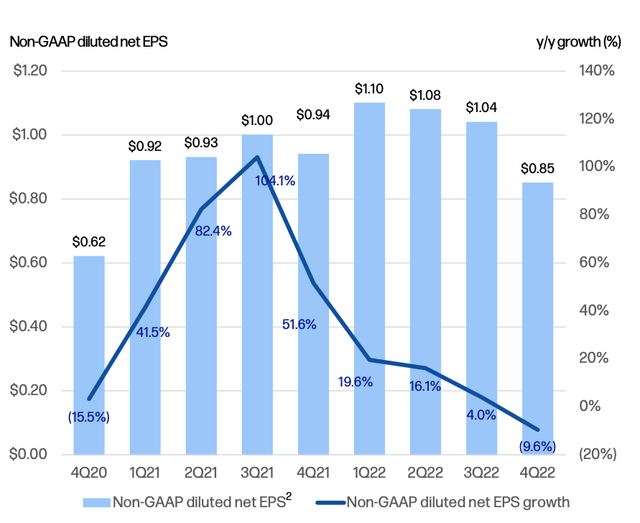

Non-GAAP operating income of $1.1 Billion was generated by HP, which fell 15% year-overyear. Non-GAAP earnings per shares were $0.85, which was down from $0.94 the previous year. This was still above analyst expectations of $0.01. Remember that the non GAAP results do not include net expenses of $855million which are mainly related to restructuring costs and one-time acquisitions. Non-GAAPEPS increased by 8% for the entire year 2022 to $4.08.

Earnings per share (Q4,F22)

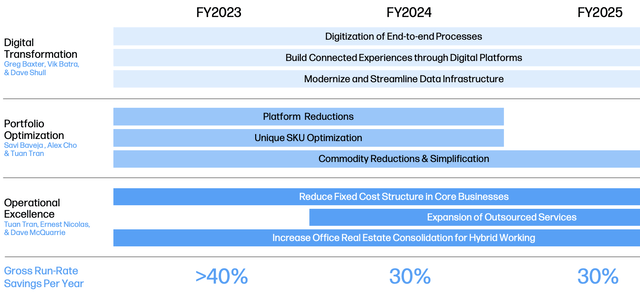

The HP Management has created a variety of cost-cutting measures to streamline the business. These include Digitization of all company processes, inventory optimization and a lower fixed cost structure. The company expects to save $1.4 billion per year through these and other activities by the end fiscal year 2023. This plan has been a success and OpEx spending has fallen by approximately $350 million over the past year.

Cost Saving Plan (Q4,FY22 report)

The company generated $3.9 billion in free cash flow over the year, and paid $5.3 billion back to shareholders through stock buybacks or dividends. HP pays a 3.4% dividend which has grown in the last 11 years.

The company’s balance sheet is solid with cash and cash equivalents of $3.145 billion and short-term investments in excess of $17 million. HP has $10.8 billion in long term debt, but only $218 millions of that is current debt.

Advanced Valuation

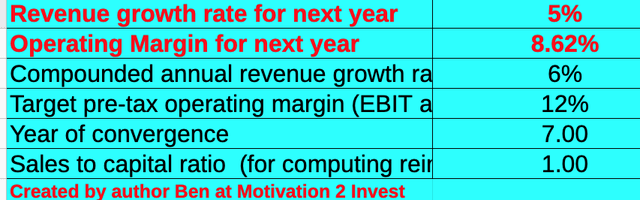

To value HP I have used the latest financials to build my advanced valuation model that uses the discounted-cash flow (“DCF”) method. As the personal computing segment recovers, I forecast a conservative 5% growth in revenue for next year.

Valuation of HP stock (Created by Ben, Motivation 2 Invest).

To increase the accuracy of the valuation I have capitalized R&D expenses, which has lifted the operating margin. Given the company’s strict cost-cutting strategy, I expect the operating margin will increase to at least 12% over the next seven years.

HPQ stock valuation 1 (created and maintained by Ben, Motivation 2 Invest).

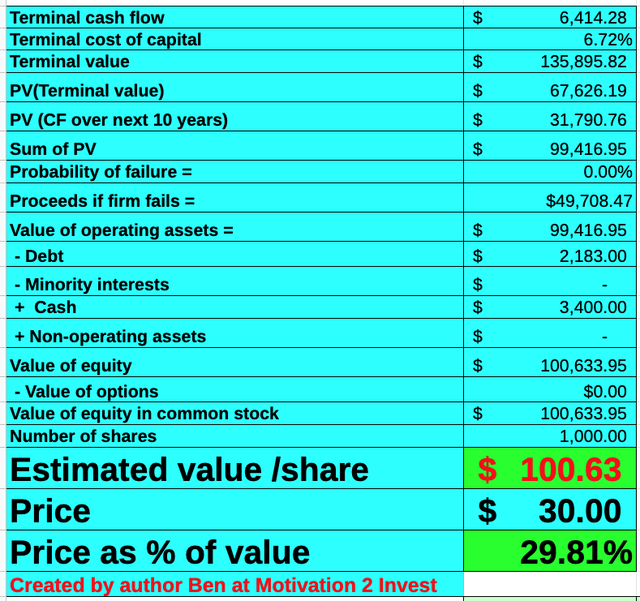

These factors give me a fair price of $100 per share. HP stock is 30% undervalued at $30 per Share at the time this article was written.

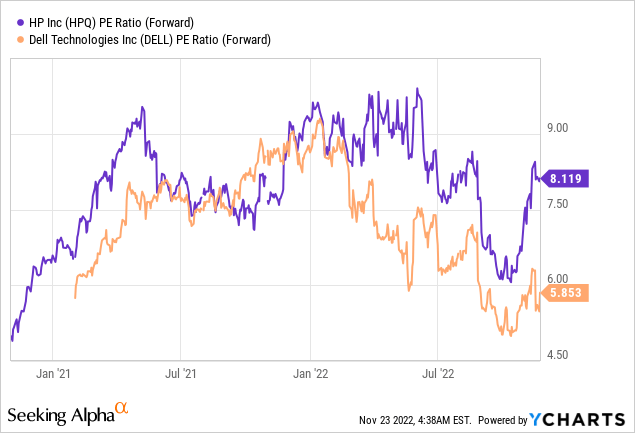

HP trades at a Forward Price to Earnings ratio (8.5), which is 10% less than its 5-year average. Comparatively, HP trades at a lower valuation than Dell (DELL), which makes it an interesting datapoint.

There are risks

Recession/Cyclical PC Supply

Many analysts predict a recession because of the high inflation rate and rising interest rates. Companies in the personal computer sales business are experiencing a downturn, which makes it difficult to survive a recession. My personal belief is that HP’s small segment Print (3% of revenue) is in a declining sector. This is because I believe the need for physical paper is less than it was 10 years back, due to the reasons discussed prior (esignatures, etc.). We also have to consider the environmental impact of printing a lot of paper. 3D printing has been growing rapidly, which could help HP retain its crown.

Final Thoughts

HP Inc. is a legacy tech company and is currently facing several short-term headwinds, including the cyclical fall in computing and unfavorable FX currency rates. The HP management is very proactive and their bold cost-cutting plays should pay dividends in the long term. These factors, combined with the stock’s low valuation, make HP Inc. a good long-term investment.